Summary

- Management was comfortable raising leverage despite the challenging environment for mortgage REITs.

- DX hedged against some of their prepayment risks by including a large allocation to CMBS in the portfolio.

- Most mortgage REITs already announced dividend reductions. DX is included within that group, but shares are attractively priced today.

- This idea was discussed in more depth with members of my private investing community, The REIT Forum. Start your free trial today »

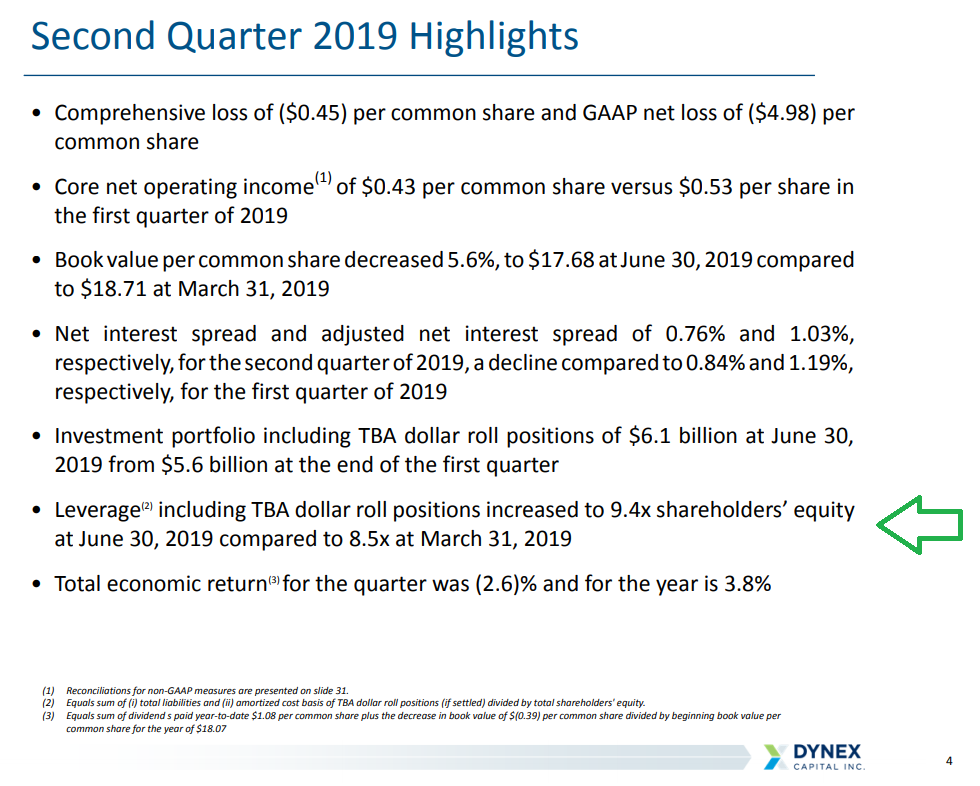

Dynex Capital (DX) took leverage up a notch in Q2 2019 compared to Q1 2019. They ended with leverage at 9.4x compared to 8.5x at the end of Q1.

Source: DX Investor Presentation

While agency mortgage REITs can push leverage even higher (into the low teens or so), it is extremely rare. Relative to the last few years, we believe the spreads between MBS and hedges are pretty attractive. That's generally a positive situation for raising leverage. However, we have to highlight that spreads are wider relative to the last few years, not relative to the last 7 or 8 years. We don't expect to see spreads on MBS get much wider than they are today (August 7, 2019).

Prepayment Risk

DX indicated that they wanted to reduce prepayment risk over the coming years. RMBS (Residential Mortgage-Backed Securities) face a significant risk from prepayments. When interest rates fall, more homeowners decide to refinance their mortgage. The owner of the MBS is paid $100 in principal for each $100 that was refinanced, but the fair value may have been higher (say $102 to $104).

On the earnings call, management highlighted that even "specified pools" (RMBS which tend to prepay at slower rates) would still be subject to prepayments if rates fell much further. To reduce their exposure, they increased the portion of their allocation allocated to CMBS (Commercial Mortgage-Backed Securities):