Summary

- Discovery Communications reported stellar second-quarter financials including free cash flow up 14% to $596 million.

- At this rate, the company will produce $2.2 billion in free cash flow for the year, or 10% of its fully diluted market value.

- Discovery's $1 billion buyback program and low valuation make the stock very attractive.

- My valuation of the stock is $44.48 per share, 49% higher than the stock price on August 7.

Discovery Communications Produced Impressive Free Cash Flow for Q2 2019

Discovery Communications (NASDAQ:DISCA) delivers over 8,000 hours of original programming available in 220 countries, including the Discovery Channel, HGTV, Food Network, TLC, Investigation Discovery, Travel Channel, Animal Planet and OWN: Oprah Winfrey Network. As I pointed out in my article last month, "Discovery Communications Is Severely Valued," the stock is very cheap. This article is a follow-up report analyzing the recent Q2 2019 results reported on August 7, 2019.

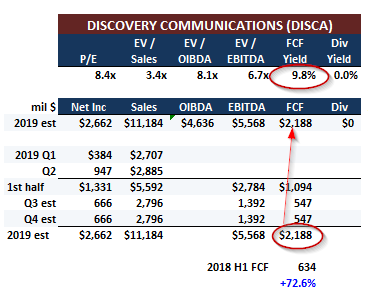

The bottom line is that free cash flow ("FCF") increased 14% during Q2 2019 over 2018, and was up 72% in the first half of 2019. At this rate, my estimate is that DISCA will produce FCF of $2.2 billion in 2019. The stock has a very attractive FCF yield of 10%. Here are my valuation estimates:

Source: Hake estimates based on the company's SEC filings

Discovery's financial condition is now very solid. DISCA took on over $8 billion in debt in March 2018 for its $8.6 billion acquisition of Scripps Networks. DISCA now has $15.1 billion in net debt, after deducting $1.3 billion in cash. On a fully diluted basis, including full conversion of the convertible preferreds owned by the Advance/Newhouse interests (28.2% of the market value of the company), the enterprise value is $37.5 billion. Given DISCA's $5.5 billion in estimated EBITDA for 2019, the stock trades for just 6.7x EV/EBITDA. This calculation can be seen in the tables below: