Summary

- COF trades at 81% of tangible book value per share, despite proving it can earn double-digit returns on tangible equity even in a low-rate environment.

- COF's economic projections underlying its credit reserves are among the most conservative of the banking industry, providing room for reserve releases.

- Losses have peaked and COF should be profitable the remainder of 2020.

- This article was highlighted for PRO subscribers, Seeking Alpha’s service for professional investors. Find out how you can get the best content on Seeking Alpha here.

The 2nd quarter of 2020 was the worst economic quarter since the Great Depression. It was a global nightmare, complete with a pandemic and mass lockdowns, in addition to exceptionally large civil unrest. As an investor, one must take a longer-term perspective and grasp the opportunity to buy attractive businesses at large discounts to intrinsic value. Such an opportunity exists with the common stock of Capital One Financial (COF). The bank is well-capitalized and boasts enormous earnings power. Loan loss reserves are conservative, and the worst is now behind them. Investors looking out 2-3 years could see 40-50% total return gains from here.

COF has a large amount of credit exposure in some of the hardest hit areas of this recession such as energy, credit cards, and auto loans. The actual credit performance though has been good, bolstered by government stimulus and deferment measures. The progression between stimulus and government assistance, to jobs and economic growth will be critical, but COF is now reserved for an immensely draconian scenario. CECL accounting front-loads the loan losses, setting up the stage for earnings growth to gain momentum soon.

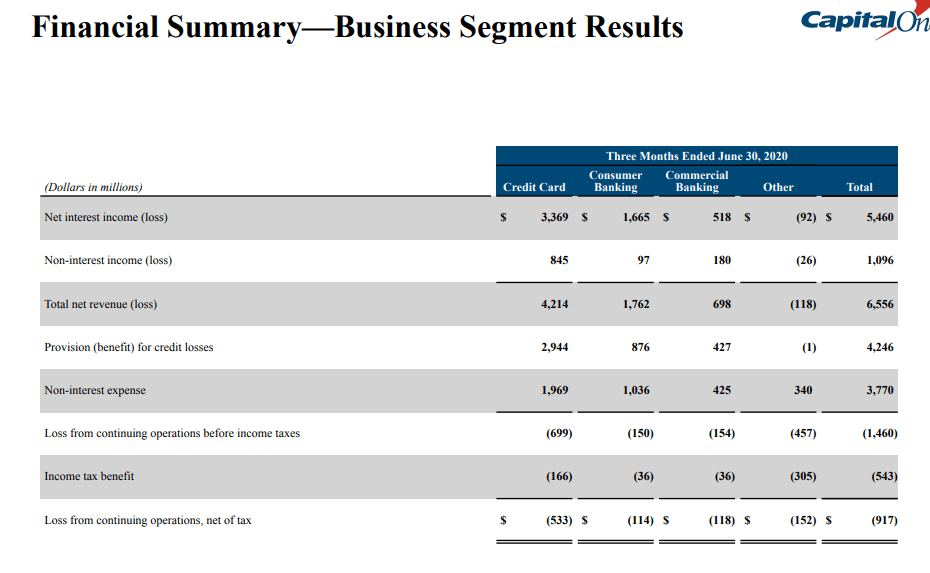

Source: COF 2Q Investor Presentation

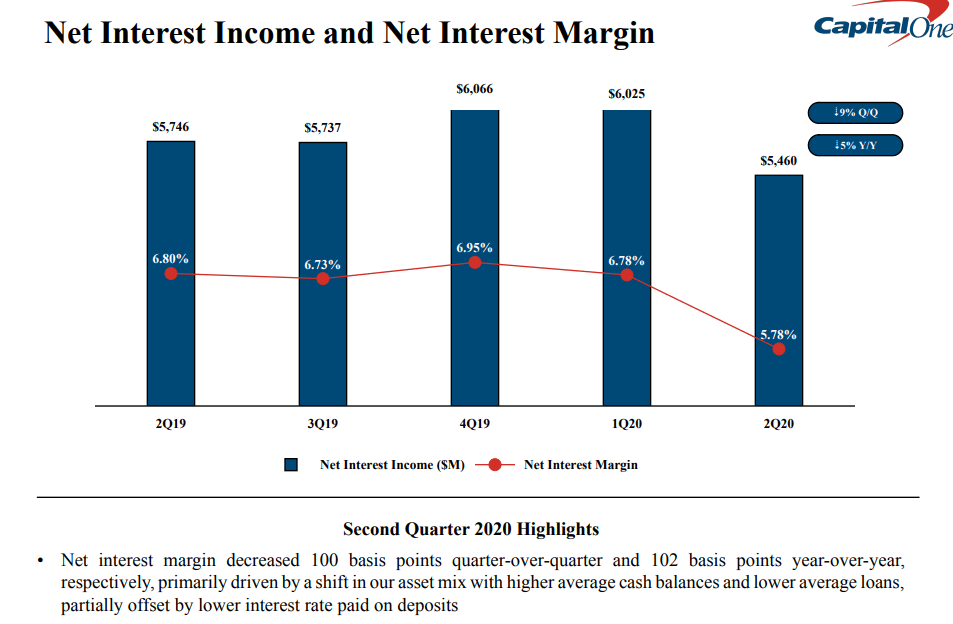

On July 21st, COF reported a net loss for the 2nd quarter of $918MM, or $2.21 per diluted common share. Adjusted losses were $1.61 per share. Pre-provision earnings decreased 21% to $2.8 billion, while the provision for credit losses was a hefty $4.2 billion. Net interest margin decreased 100 basis points QoQ and 102bps YoY, respectively, due to higher average cash balances and lower average loans, partially offset by lower interest rate paid on deposits. This quarter should represent the trough on net interest income and NIM should improve as well, as the company reduces its cash holdings into higher yielding loans and investments.