Summary

- Gannett’s financial ratios and key indicators did not improve a material amount based on the Q2 2020 quarterly report.

- Gannett’s theoretical return to pre-COVID net income margins would still mean trouble for the company in the long term.

- Gannett is competing in a dying industry that is being bombarded by free alternative news outlets and increased competition from the big players.

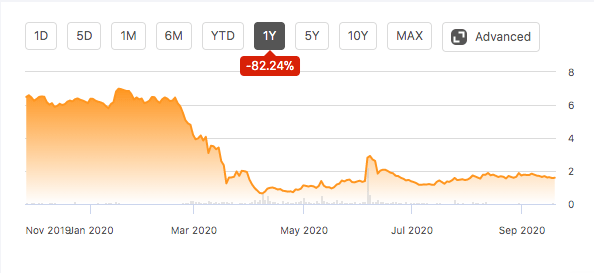

Gannett (NYSE:GCI) is a modern media company that owns several print and digital news brands, including USA Today. Gannett’s stock price has seen a historical tumble in the past few years, driven by the fact that the company took on an insane debt agreement in 2019, and the newspaper industry is slowly on the decline.

(Gannett Co. Stock Market Chart, Seeking Alpha)

Gannett’s Q2 2020 report spilled more trouble

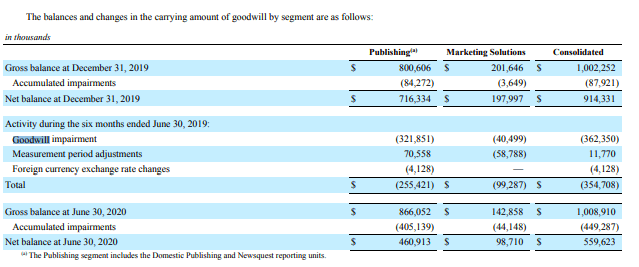

One of the most notable changes in the recent quarterly report is that Gannett wrote down a significant amount of goodwill. A total of around $362M to be exact, down from $914M, which is quite significant considering that this write-down contributed largely to the company’s drop in total asset values of about 17%. $321M of the total goodwill write-down is related to the Publishing reporting unit, which is quite concerning as based on the company’s future outlook, its own acquisitions are expected to see a significant decline in future benefits moving forward (Gannett 10-Q, 2020).

We believe that in the next few quarters, Gannett will continue to write down the current goodwill amount of around $559M. Its goodwill calculations were based on “current and expected future economic conditions (Gannett 10-Q, 2020)” and acknowledged that “the newspaper industry and the company have experienced declining same-store revenue and profitability over the past several years, and these industry trends are expected to continue in the future (Gannett 10-Q, 2020).” This is important given that investors may be deceived by the company’s current asset-to-liability ratio, and we expect to see this ratio decline over the next few years. Tangible assets are much more valuable when trying to consider whether or not a company can take on large loads of debt, and in this case for Gannett, around $1.6B.

(Gannett 10-Q, 2020)

While examining the operating revenues for Q2 2020, investors should not be deceived by the dramatic increase in the revenue figure but should note that overall, same-store revenues actually fell a staggering 28% compared to last year (Gannett 10-Q, 2020). Gannett noted that for June, same-store revenues were only down 24% compared to the prior year, and the company expects this figure to improve in Q3. We believe that same-store revenues will fail to reach 2019 figures for at least another year due to the vulnerable state of the economy.