Summary

- Having raised its dividend every year since the Kennedy administration, Johnson & Johnson is on the prestigious Dividend Kings list.

- Despite the risks of being a scapegoat of the opioid crisis and the ongoing talc-based product lawsuits, Johnson & Johnson boasts the distinction of an AAA credit rating.

- In addition, the company is likely to benefit from increased healthcare spending as the world grows wealthier, larger, and older. Johnson & Johnson also possesses a proven management team.

- Unfortunately, the company is trading at a 9% premium to my estimated fair value and at a 4% premium to my target price.

- Between the 2.7% yield, 6-7% earnings growth, and 0.4% valuation multiple contraction, Johnson & Johnson will likely deliver annual total returns of 8.3-9.3% over the next decade.

With the S&P 500 soaring 19.1% year to date, it is becoming increasingly difficult to find companies that are trading at a reasonable valuation.

As a dividend growth investor, I am always looking to add to my positions in the tried and true dividend growth companies operating in necessary and growing industries. Unfortunately, most of those companies are overpriced at this point, and one such name that I believe is a bit too overpriced is Johnson & Johnson (JNJ).

I'll be discussing Johnson & Johnson's dividend safety and growth profile, fundamentals, and valuation. I'll also offer my predictions for annual total returns at the current price for the next decade. I'll then conclude by offering the target price Johnson & Johnson shares would need to drop to before I would consider adding to my position.

Johnson & Johnson Offers A Fantastic Blend Of Dividend Growth And Dividend Safety

I tend to prefer companies that offer a mix of dividend growth and dividend safety. After all, while dividend safety is great, it's utterly worthless if it comes with no dividend growth because inflation will slowly eat away at the purchasing power of the dividends you receive. But at the same time, a company growing its dividend at a much faster rate than it's growing its earnings signals that the dividend may eventually be at risk of a cut if the company encounters difficult times and has an elevated payout ratio.

I'll examine Johnson & Johnson's dividend safety using both the EPS payout ratio and the FCF payout ratio for its last fiscal year.

During FY 2018, the company generated $8.18 in adjusted EPS against dividends per share of $3.54 during that same time period, for an EPS payout ratio of 43.3%.

According to page 15 of Johnson & Johnson's most recent 10-K, the company generated operating cash flow of $22.201 billion against capital expenditures of $3.670 billion, for total FCF of $18.531 billion. When we factor in that the company paid $9.494 billion in dividends last fiscal year, this equates to a very safe 51.2% FCF payout ratio.

Overall, we can see that both the company's EPS and FCF payout ratios are very safe.

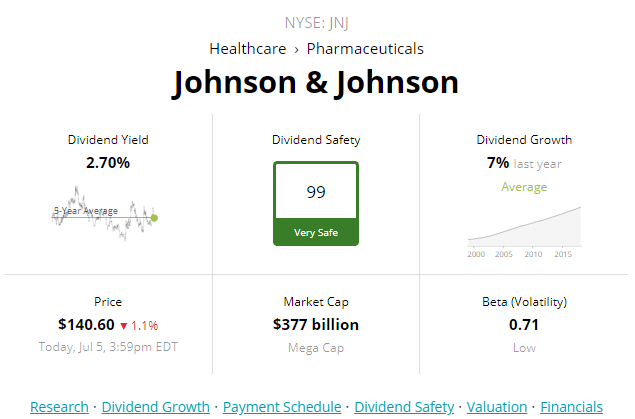

Image Source: Simply Safe Dividends

Unsurprisingly, Simply Safe Dividends and I agree that Johnson & Johnson's dividend is as safe as they come.

The next logical consideration for us is the dividend growth potential of the company's dividend.