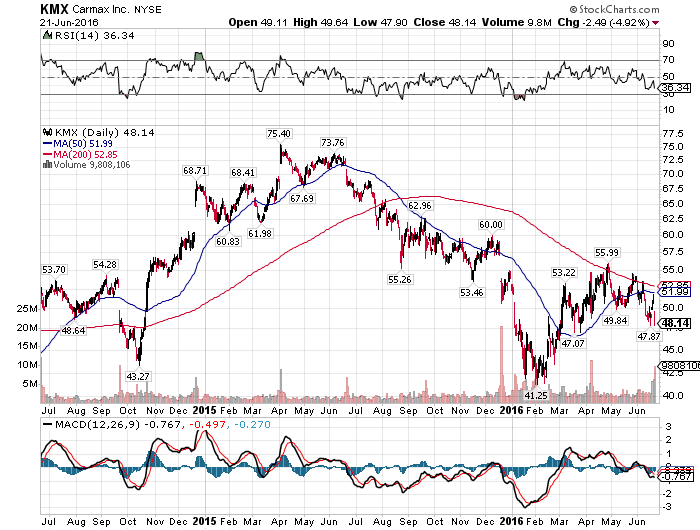

CarMax (NYSE:KMX) has done a terrific job in the last several years of carving out a niche for itself in the car retailing business, and it has no doubt become a dominant player. But investors were far too excited about KMX's prospects for much of 2015, bidding the stock up into the mid-$70s. That created a situation where KMX was undoubtedly overvalued, and even a couple of months ago - after the Q4 report, I said KMX was still too expensive. KMX's Q1 report came out yesterday and the results were weak, confirming my downside bias from earlier this year. Shares were down moderately on the news, but with KMX back in the high $40s, is there yet more room to the downside?

My concerns over KMX's valuation stemmed from a lack of comparable revenue growth that started to creep in last year and waning margins that comes along with weaker sales. KMX had both of these issues in Q4, but in Q1, the picture was a little more mixed.