Summary

- Since demerging from Altria in 2008, Philip Morris has seen liabilities rise significantly faster than assets. Technically their balance sheet has thus become insolvent.

- Whilst this may sound alarming, given their strong liquidity and ability to service their debt there are no reasons to be concerned.

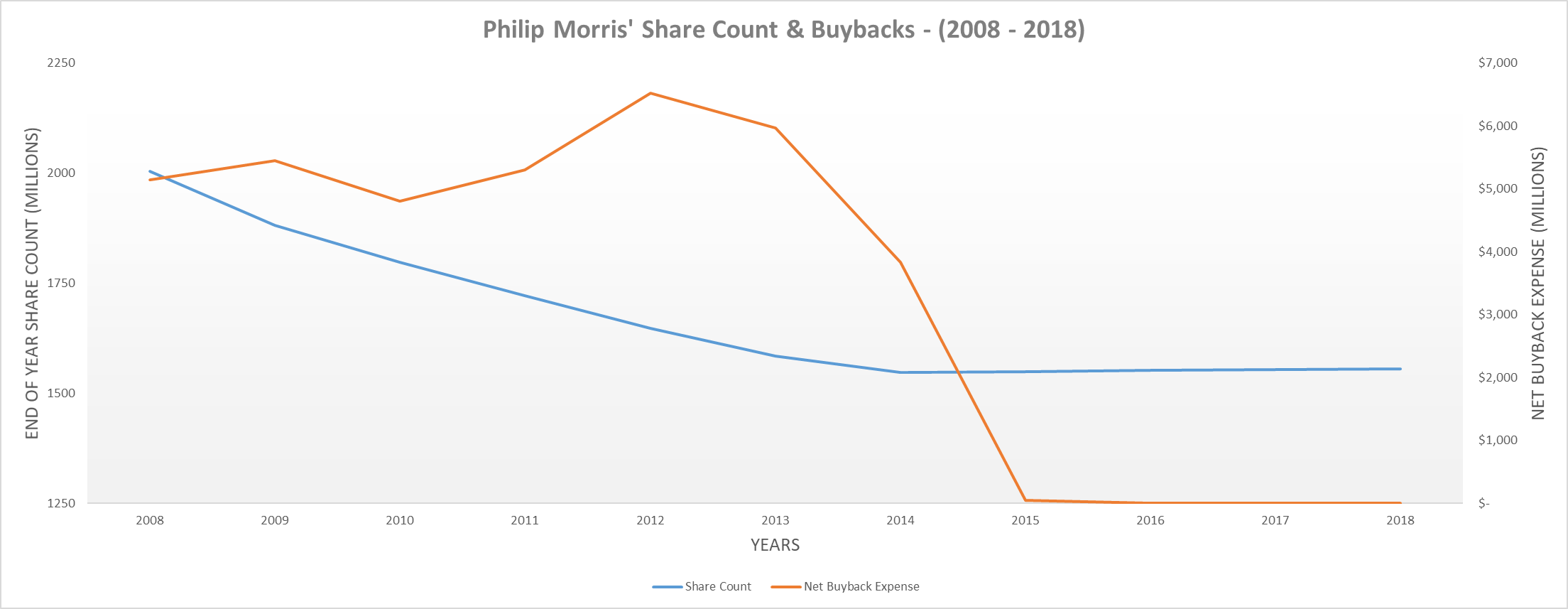

- The primary cause of the soaring liabilities is from the new debt issued to conduct share buybacks.

- Even though overall these buybacks have produced a positive return, it's rather low considering the length of time since they were conducted.

Introduction

One of the phrases that normally strikes the most fear in the heart of both debt and equity investors is insolvency, as it normally foretells significant financial losses on the horizon. Given the blue chip dividend status commonly attached to Philip Morris (PM), it may surprise some investors to learn their balance sheet is technically insolvent. Whilst this may sounds scary and deter some potential investors, there are actually no significant reasons to be concerned.

Background

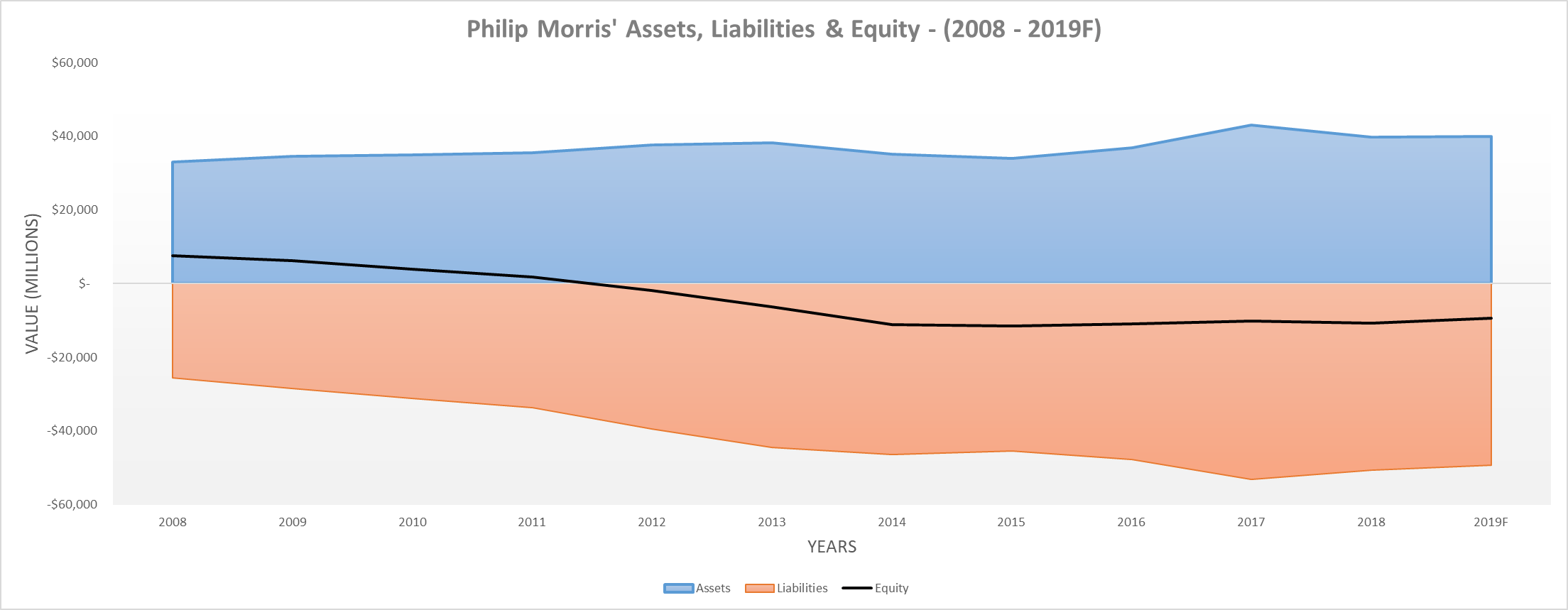

Image Source: Author.

Since demerging from Altria (MO) they have seen their assets grow 21.08% from $32.972b at the end of 2008 to $39.923b at the end of the latest second quarter. Meanwhile their liabilities have grown 93.67% from $25.472b to $49.332b during the equivalent time period, causing their equity to fall to negative $9.409b and thus technically meaning they’re balance sheet is insolvent.

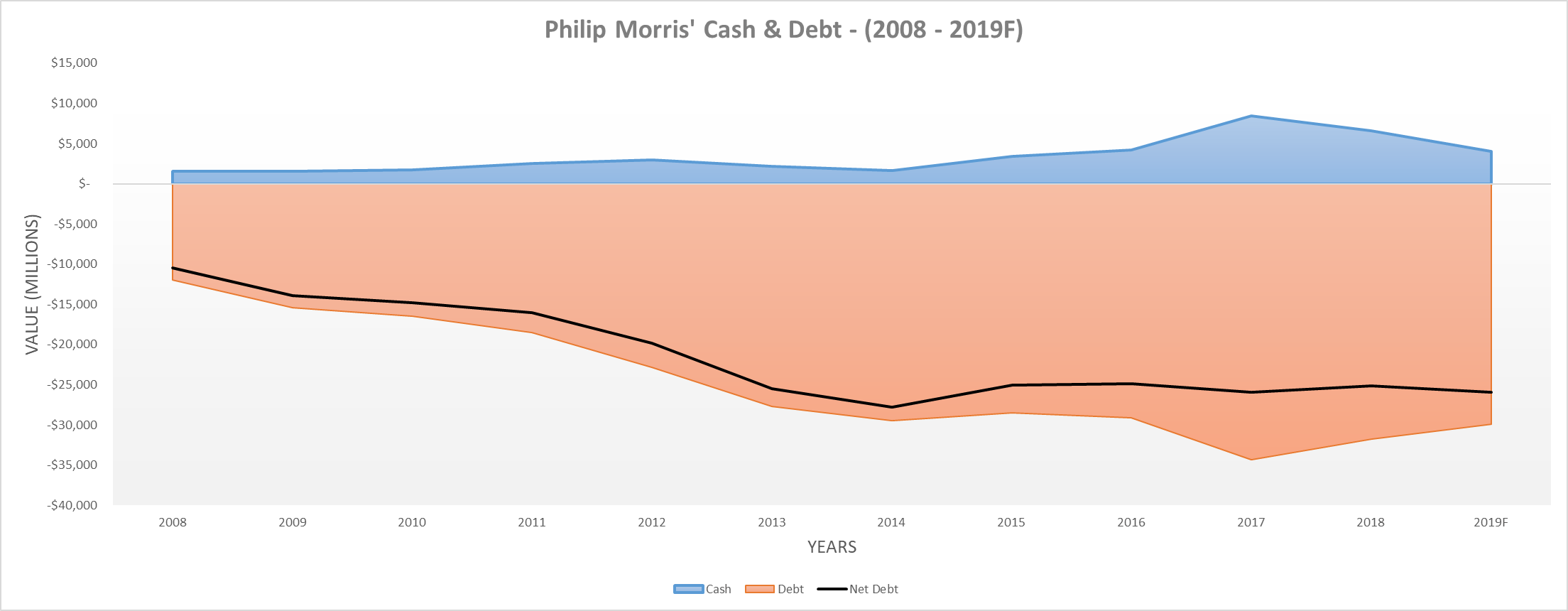

Image Source: Author.

The primary cause for this rapid expansion of liabilities stems from their debt increasing 149.89% from $11.961b at the end of 2008 to $29.889b at the end of the latest second quarter. The majority of this debt was used to fund their share buybacks that ultimately ceased following 2014.