Summary

- Having raised its dividend for the past 17 years, Lockheed Martin is a Dividend Contender.

- Despite the inherent risk of being the leading defense contractor, Lockheed Martin is a well-managed defense contractor with a strong balance sheet.

- Adding to the case for an investment in Lockheed Martin is the fact that the company is trading at what I believe to be fair value.

- Between Lockheed Martin's 2.5% yield, 7-8% earnings growth, and a static valuation multiple, Lockheed Martin is likely to deliver annual total returns of at least 9.5-10.5% over the next decade.

- It's for these reasons that I'm proud to announce I have finally opened in a position in Lockheed Martin.

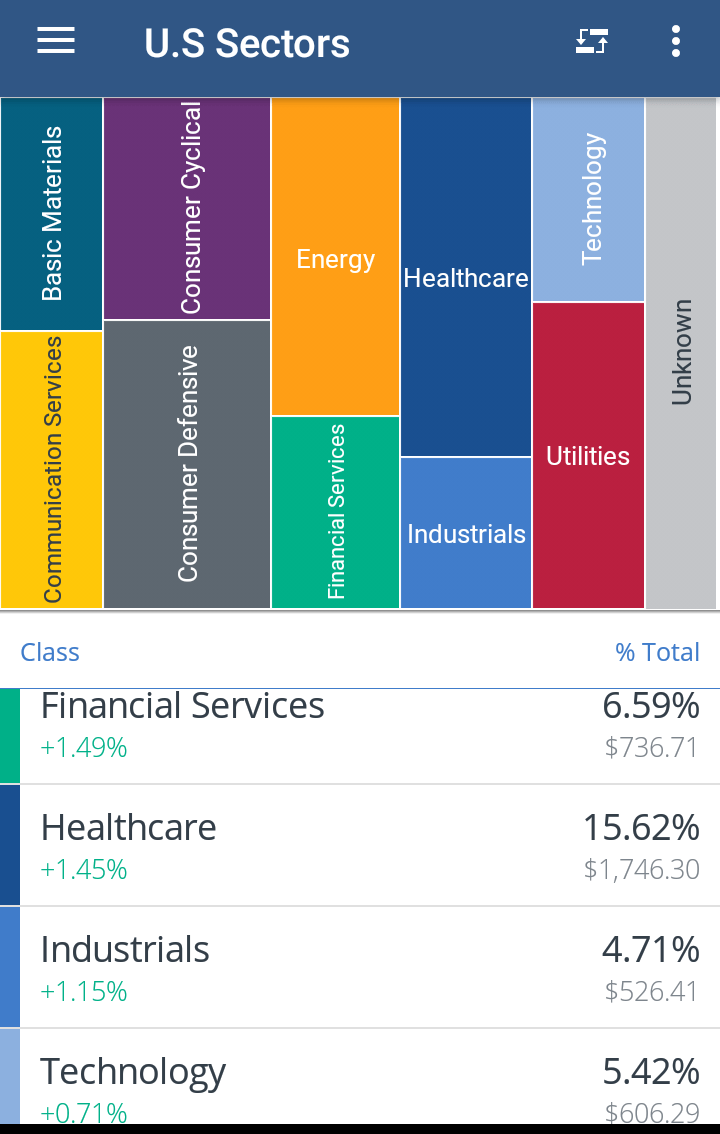

As I discussed in my article on Wells Fargo last week, there are a few sectors that I would like to increase my allocation to in the years ahead. Specifically, I'd like to increase my allocation and diversification within the financial services, industrials, and technology sectors to an extent.

Image Source: Personal Capital

Image Source: Personal Capital

I took yet another step toward increasing my exposure in financials and industrials. Aside from the position that I initiated in Wells Fargo last week, I also initiated a position in Lockheed Martin (LMT). As a side note, I'll also be detailing my other purchases for the month of October in a few weeks.

Today, we'll analyze Lockheed Martin's dividend safety and growth profile, the company's fundamentals and risks, as well as the valuation at the current price.

I'll then conclude the article by offering my prediction of Lockheed Martin's annual total return potential over the next decade.

A Very Safe Dividend With High-Single Digit Dividend Growth Potential

As a dividend growth investor, I have found it's always prudent to examine the safety of a company's dividend, as well as the growth potential of such dividend.

We'll assess the extent to which Lockheed Martin's dividend is safe by measuring both the company's EPS and FCF payout ratios.

In its prior fiscal year, Lockheed Martin generated $17.59 in diluted EPS against dividends per share of $8.20 during that time, for an EPS payout ratio of 46.6%.

For the current fiscal year, Lockheed Martin recently raised its outlook from $20.05-$20.35 in diluted EPS to $20.85-$21.15 against dividends per share slated to be $9.00, for an EPS payout ratio of 42.9%, using the diluted EPS midpoint figure of $21.00.

Moving to the FCF payout ratios, Lockheed Martin generated $3.138 billion in operating cash flow in 2018 (which was due to an exceptionally high $5.0 billion in pension contributions in 2018 according to page 23 of Lockheed Martin's most recent 10-K) against $1.278 billion in capital expenditures, for total FCF of $1.860 billion.

Against the $2.347 billion in dividends paid during this time, Lockheed Martin's FCF payout ratio equates to 126.2%.