Summary

- While Capital One's revenue trends are encouraging, cost base inflation continues to offset this, leading to pre-provision profit stagnation. Credit costs also keep rising.

- Management prefers share repurchases over dividends. With 12% CET1, the bank can buy back $2.5B per year over 2020-21E. Quarterly dividends might remain unchanged at $0.40 per share.

- Valuation looks fair given the riskier loan book and lower return of equity dynamics.

Capital One (COF) marginally lagged Street expectations, reporting an 11% YoY drop in fourth quarter profits. While the card & auto-heavy lender reported healthy rise in pre-provision operating profits (PPOP), credit costs dampened this with an 11% jump, half of it due to the Walmart (NYSE:WMT) card portfolio acquisition. Higher effective tax rate compared to a year ago also added to the profit decline.

COF has solid CET1 levels, much above the long-term target of 11%. While it is quite feasible to hike the quarterly dividends, which have been unchanged at $0.40 per share for the past several years, the management has always preferred share repurchases over dividends. The bank can easily buy back $2.5B per year over 2020-21E. On the valuation side, COF stock looks to be fairly valued, despite being cheaper than most peers.

Margins to hold up in 2020; cost rise is a worry

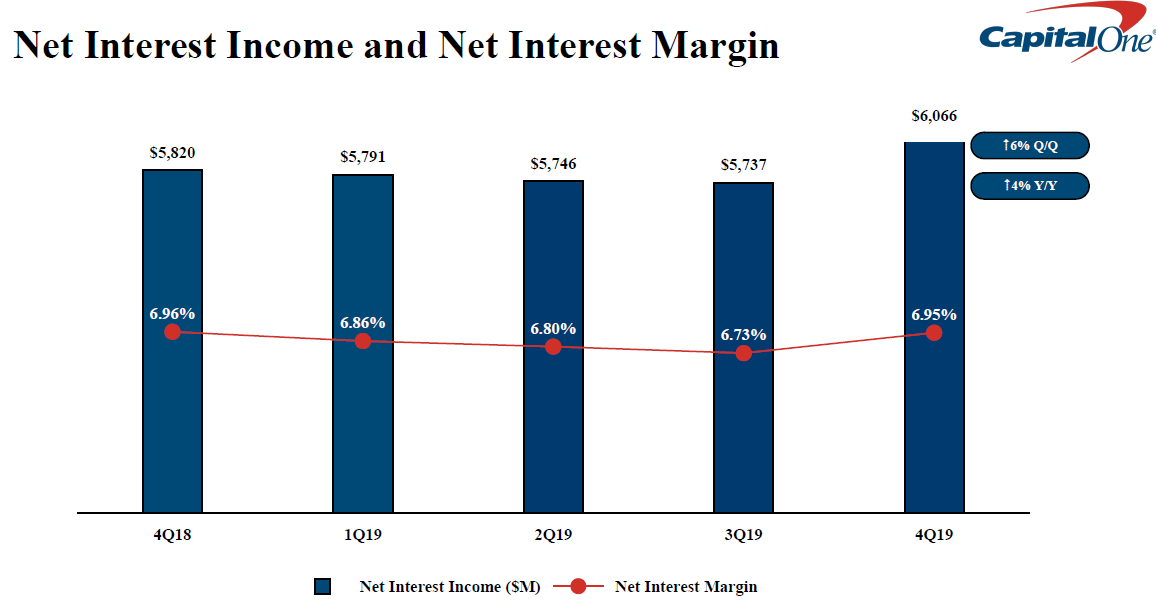

At a time when its peers are reporting net interest margin (NIM) decline, COF’s margins expanded 14bps QoQ (excluding the PPI impact from UK operations). This was primarily driven by the on-boarding of the Walmart portfolio. While this book is higher-yield, keep in mind that it is also a higher-loss one – thus, we will need to wait for a few more quarters to have a more holistic view.

Source: Company presentation

The bank is relatively neutral in terms of near-term interest rate movements, likely due to the fact that its book is dominated by credit cards and auto loans, which are not as interest-sensitive in the short term. Thus, COF is likely to show more revenue resilience than peers in 2020. However, once the rates start to rise, the bank will lag.

Loan growth was encouraging, as it rose 6.6% QoQ (+8.1% YoY). Due to the seasonality of the fourth quarter, specifically in the cards segment, it is better to look at the loan growth on a YoY basis. Out of the $20B change, $9B was contributed by the integration of Walmart's book. Organic growth - that is, excluding the WMT portfolio acquisition - loans were up 4.4% YoY, driven by commercial (+6.5% YoY), and auto (+7.1% YoY), while card (+2.1% YoY) was a bit of laggard.

Non-interest income was solid, rising 11.4% QoQ (+14.1% YoY). Fees grew 7.5% QoQ (+5.3% YoY).

Cost control has been an area where COF has been quite weak. Fourth quarter opex changes were mixed – employee costs rose 23% YoY, while occupancy (-7.4%), marketing (-14.6%), and professional services (-25.4%) spending tempered. Overall, the cost base was flattish. However, over the past few years, the bank has been exhibiting rather looser cost control, with opex rising 4-5% over 2017-19, and efficiency ratio deteriorating a full 200bps. While the revenue trends are likely to be stable to falling in the near term, a quicker rise in costs is a threat to pre-provision growth, and ultimately to net profits, given the pace at which provisions are increasing. PPOP hardly grew during 2017-19.