Summary

- Capital One is a well-run bank that has differentiated itself from the majority of other commercial banks.

- A focus on credit card lending and technology has created a strategy that is difficult to replicate and positioned the bank well to continue in the future.

- Recession fears have knocked ~30% off it's market value in the past month, and could offer solid returns in the future if the fear subsides.

Low Rates and the Shape of the Yield Curve Are Absolutely Affecting Banks

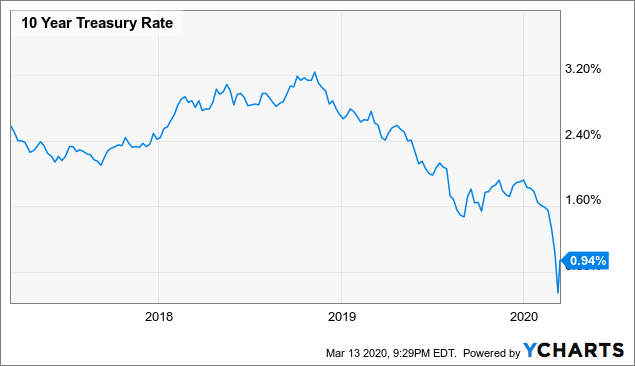

Historically low rates, a flat/inverted yield curve, and ever increasing recession fears are not great for banks to put it mildly. The Fed cut rates 50 bps in early March and the market is pricing in a ~67% probability of 75 bps cut this week. The 10 year is hovering under 1%. Banks are struggling in their search for yield. However, Capital One (COF) is unique from most regional and national banks.

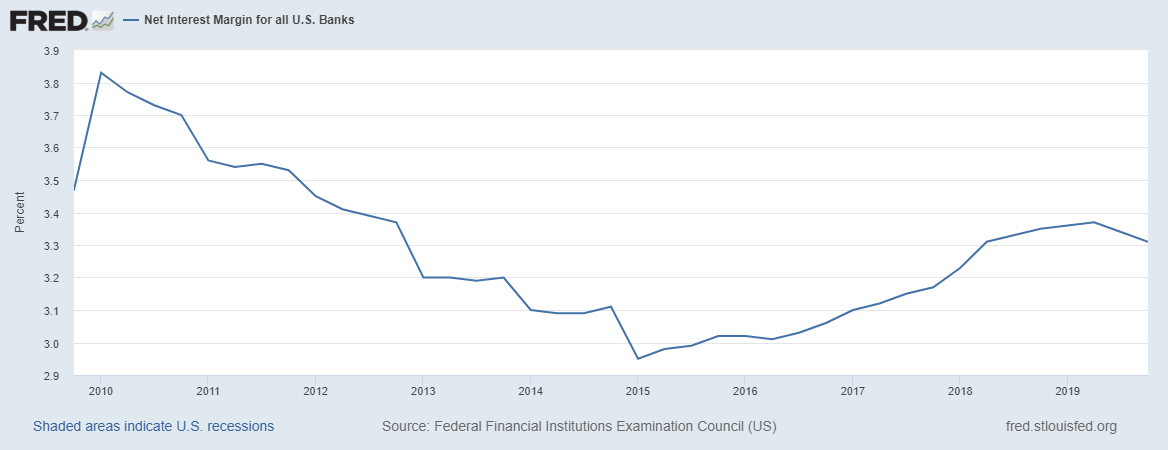

Since bottoming in early 2015, net interest margins for U.S. banks rebounded through 2019 but compressed at the end of the year. According to the Federal Reserve Bank of St. Louis, the average NIM for all U.S. banks was 3.31% at the end of 2019.

Capital One Is Different Than Most Other Banks

Capital One, on the other hand, has some of the strongest margins of any U.S. bank. At the end of 2019, the bank had a NIM of a little under 7%. This is a result of the structure of their balance sheet. Whereas the majority of banks have a heavy concentration in commercial and mortgage loans, half of Capital One's loan book is credit cards.