Summary

- Dunkin' Brands is a growing, capital-light franchisor in the attractive beverage-led Quick Serve Restaurant space.

- The business has ample room to replicate its model in the western part of the U.S.

- The core business should compound intrinsic value per share at low double-digits annually for several years.

- Shares trade at a modest discount to historical valuations and could become quite attractive given a moderate pullback.

If someone new to investing were to ask me where to start when trying to find potential investments, I would first recommend studying predictable, free cash flow generative businesses with an entrenched competitive position. I can't value a business when I can't reasonably estimate the cash the business will generate over the next 5+ years, and I am only interested in owning growing, above-average businesses that tend to display the above characteristics. Secondarily, but of no less importance, is to pay a price for that business that affords a margin of safety in case some of your assumptions are off the mark.

We try to spend most of our time researching businesses that meet these criteria, and here I'll take a look at Dunkin' Brands Group Inc. (NASDAQ:DNKN), owner of the Dunkin' and Baskin-Robbins franchises and a business that scores highly on many of these marks.

Dunkin' is a capital-light business serving a loyal and habitual customer base. Despite occupying one of the leading positions in the caffeinated beverage market, the business is considerably under-penetrated in the western half of the U.S. This, combined with recent success in its mobile and loyalty program, which were accelerated by the pandemic, should lead to low double-digit compounding in intrinsic value per share for several years.

Business Overview

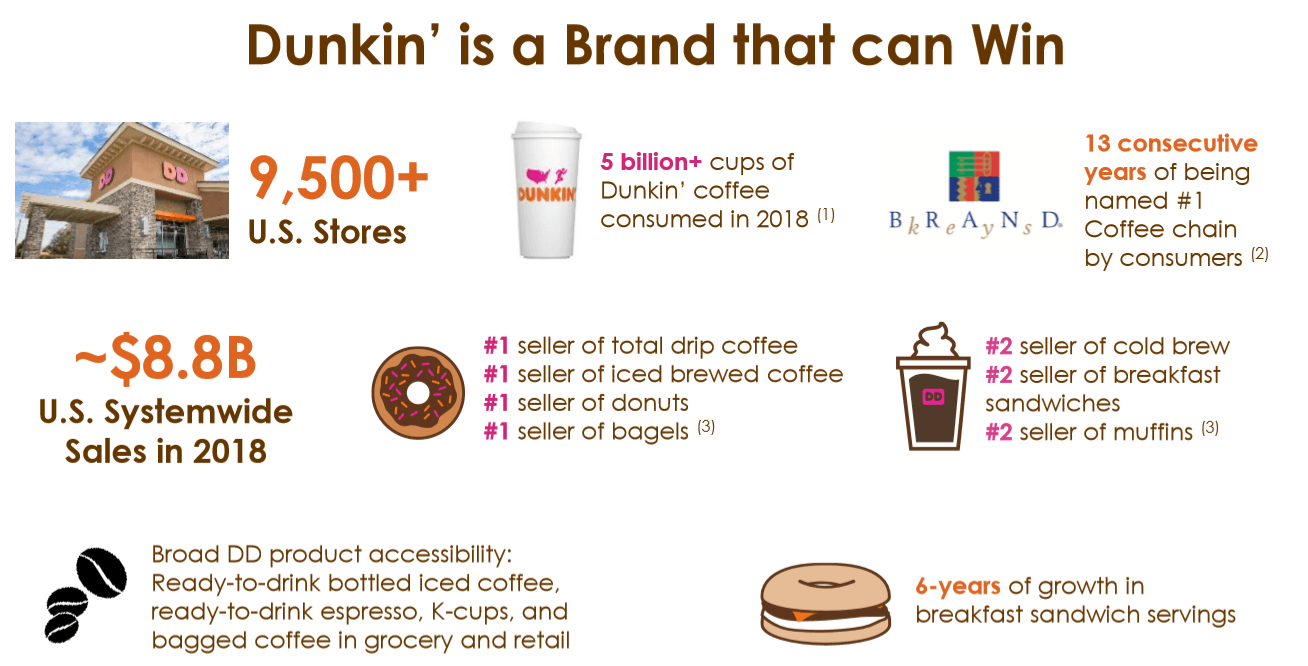

Dunkin' employs a simple, 100% franchised operation with a presence in 60 countries and over 21,000 locations. Their Dunkin' brand occupies a leading position in hot and cold coffee, donuts, bagels, and breakfast sandwiches in the U.S. while Baskin-Robbins offers premium ice cream options primarily abroad.

Source: 2019 Q3 Investor Presentation

While ~17% of segment revenue comes from Baskin-Robbins and Dunkin' International, the long term growth and profitability driver is Dunkin' U.S (~85% of segment profits), and accordingly is where I'll spend the bulk of this article.

The Dunkin' brands' roots trace back to the 1940s and compete in the Quick Serve Restaurant (QSR) space against the likes of Starbucks, Burger King, Panera, Wendy's, and many others. Originally focused on breakfast foods, since the 1980's Dunkin' has transformed into a beverage-based concept and a national leader in the coffee category with over 5 billion cups of Dunkin' coffee consumed in 2018. After going through a stint of private equity ownership by Bain Capital, the Carlyle and Thomas H. Lee Partners, the company IPO'd in 2011. Since going public the shares have returned high-teens annually (through 2019), comfortably outpacing the S&P 500 over the same period.