Summary

- COVID-19 had no material impact on Lockheed Martin’s business, and with more than $140 billion worth of deals in its backlog, the company will thrive in the current environment.

- By being a defense contractor, the economic downturn will not affect Lockheed Martin, and the company’s EPS for 2020 is forecasted to be $24.11 per share.

- We consider the stock to be one of the most attractive, pandemic-resistant long-term plays on the market right now.

COVID-19 had no material impact on Lockheed Martin (LMT). With more than $140 billion worth of deals in its backlog, the company will thrive in the current environment, and its business could be considered pandemic-proof. As the US annual defense budget is expected to increase from $676 billion in 2019 to $906 billion by 2030, Lockheed Martin, as Pentagon’s biggest contractor, will undoubtedly benefit from such growth. While there’s a risk that the company could lose some of its foreign orders from the oil-rich Gulf states, which are currently suffering from the low oil price environment, Lockheed Martin will be able to offset all of those losses by winning additional defense contracts from the Department of Defense. At the same time, with more than $10 billion in debt, the company is not going to have a liquidity crisis anytime soon, as its EBIT could cover its interest expenses 13 times over. By trading at P/E of 16x, we consider Lockheed Martin to be one of the best aerospace stocks on the market right now with the potential to create value in the long run. For that reason, and because of the fact the company will be able to sustain its dividend payments with a payout ratio of more than 40% for a long time, we opened a long position in Lockheed Martin.

More Room For Growth

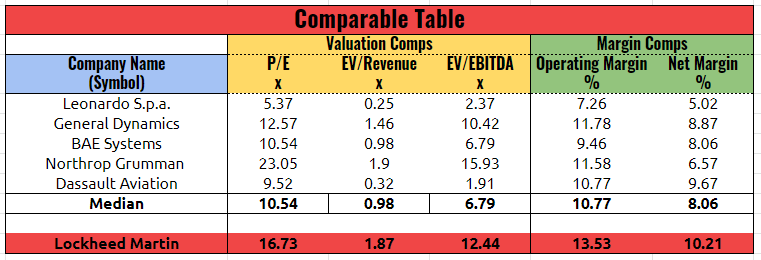

While the US economy entered a recession in the first half of the year and recorded the largest unemployment rate in its history, Pentagon’s biggest contractor Lockheed Martin said that the pandemic had no material impact on its business. In Q1, its revenues of $15.69 billion were up 9.4% and its GAAP EPS of $6.08 were above analysts’ estimates by $0.28. By being a defense contractor, Lockheed Martin will always outperform its civil aerospace peers during economic downturns. While companies like Boeing (BA) and Airbus (OTCPK:EADSF, OTCPK:EADSY) are experiencing order cancellations for passenger planes on a massive scale, Lockheed Martin’s businesses from aeronautics, missile and fire control, and rotary and missions systems fields are all experiencing double-digit growth. We could see from the table below that even when compared to other defense contractors, Lockheed Martin is also able to outperform them, as its operating and net margins of 13.53% and 10.21%, respectively, are above the industry’s median margins.

Source: Capital IQ

Thanks to its technical advantages against others, Lockheed Martin will continue to receive new orders from the Department of Defense and create value for its shareholders. In June, the company won a contract worth $1.04 billion for the production of guided missile systems, and just recently, it was awarded $15 billion to develop C-130J transport aircraft for the U.S. Air Force. The defense industry will continue to be the most crucial part of the national security strategy of the United States, and the country’s annual defense budget could grow to $906 billion in 2030, a 34% increase from $676 billion in 2019. The government always has much deeper pockets than businesses and consumers, and as a result, companies like Lockheed Martin, which are also crucial for the United States national security, are always going to be great investments even in turbulent times.